Structural Time Series Models

STSmodel.RdTools for Structural Time Series Models, as described e.g. in (Harvey 1994) .

Value

Model template, i.e. a list with slots

h\(((m+s)(n+s) + m^2)\)-dimensional vector,

H\(((m+s)(n+s) + m^2, k)\)-dimensional matrix,

classclass = "stspmod", only state space models are implementedorderorder = c(m,n,s)(output, noise and state dimensions),n.parnumber of free parameters \(=k\) and

idxa list with slots

state,noiseandpar. These indices code which states, noise components and parameters are associated to the respective components. See the example(s) below.

Details

Local Level Model (LLM): tmpl_llm()

$$a_{t+1} = a_t + u_t,\quad y_t = a_t$$

where \((u_t)\) is white noise with variance \(\sigma_u^2\).

The model has one free parameter \(\theta = \sigma_u\).

The output process \((y_t)\) is a random walk.

Local Linear Trend Model (LLTM): tmpl_lltm()

$$a_{t+1} = a_t + b_t + u_t,\quad b_{t+1} = b_t + v_t,\quad y_t = a_t$$

where \((u_t)\), \((v_t)\) are two independent white noise processes

with variance \(\sigma_u^2\) and \(\sigma_v^2\).

The model has two free parameter \(\theta_1 = \sigma_u\)

and \(\theta_2 = \sigma_v\). In general the output process is

integrated of order two (\(I(2)\)). For \(sigma[v]^2=0\)

the model generates a random walk with drift and for \(sigma[u]^2=0\)

one gets an integrated random walk.

Cyclical Models: tmpl_cycle(fr, rho)

tmpl_cycl(fr. rho) generates a template for scalar AR(2) models, where

the AR polynomial has two roots at

$$z = \rho^{-1}\exp((\pm i 2\pi f)$$

If the "damping factor" \(\rho\) is close to one then the model generates

processes with a strong "cyclical component" with frequency \(f\).

For \(\rho <1\) the AR(2) model satisfies the stability condition, i.e.

the forward solution converges to a stationary process. For \(\rho > 1\)

the trajectories of the forward solution diverge exponentially.

The template has one free parameter, the standard deviation of the driving white noise:

\(\theta = \sigma_u\).

Seasonal Models: tmpl_season(s)

tmpl_season(s) generates a template for scalar seasonal models, i.e.

for models which generate trajectories which are "almost" periodic

with a given period, \(s\) say. The template has one free parameter,

the standard deviation of the driving white noise:

\(\theta = \sigma_u\).

Combine Models cbind_templates(...)

The utility cbind_templates(...) may be used to construct

models from simple "bulding blocks". Suppose e.g. that the observed process is

described as the sum of two (unobserved) components

$$y_t = k_1(z) u_t + k_2(z) v_t$$

where \((u_t)\), \((v_t)\) are two independent white noise processes.

If both components are described by the templates tmpl1 and tmpl2

then we may construct a template for the combined model simply

by cbind_templates(tmpl1, tmpl2).

The function cbind_templates only deals with state space models and

of course all templates must describe outputs with the same dimension.

The functions tmpl_llm(), ..., tmpl_season() generate templates

for scalar time series. However, the utility cbind_templates(...)

also handles the multivariate case.

References

Harvey AC (1994). Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge University Press, Cambridge.

See also

See model structures and local model structures for more details on model templates.

Examples

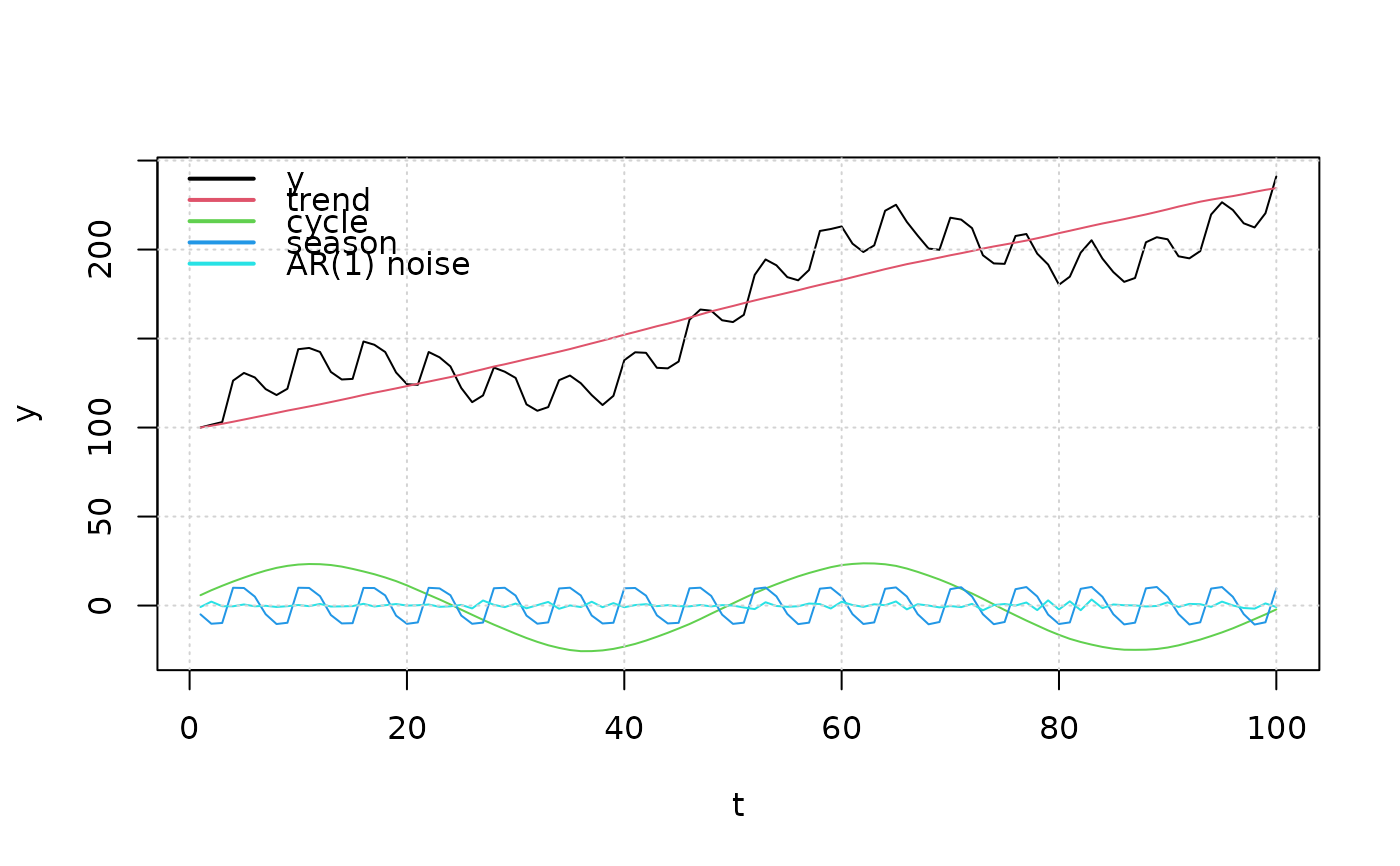

# build a structural times series model (see Harve 94) with

# a "local linear trend component",

# a cyclical component with period 50 (frequency 1/50),

# a seasonal component with period 6 and

# an AR(1) component.

tmpl = cbind_templates(tmpl_lltm(), tmpl_cycle(1/50,1), tmpl_season(6),

tmpl_stsp_ar(1, 1, sigma_L = 'identity'))

# set some "reasonable" values for the standard deviations

# of the respective noise and for the AR(1) coefficient.

model = fill_template(c(0.0, 0.1, # parameters for trend (lltm) component

0.1, # parameter for cyclical component

0.1, # parameter for seasonal component

-0.5 # AR(1) coefficient

), tmpl)

print(model)

#> state space model [1,5] with s = 10 states

#> s[1] s[2] s[3] s[4] s[5] s[6] s[7] s[8] s[9] s[10] u[1] u[2] u[3]

#> s[1] 1 1 0.000000 0 0 0 0 0 0 0.0 1 0 0

#> s[2] 0 1 0.000000 0 0 0 0 0 0 0.0 0 1 0

#> s[3] 0 0 1.984229 -1 0 0 0 0 0 0.0 0 0 1

#> s[4] 0 0 1.000000 0 0 0 0 0 0 0.0 0 0 0

#> s[5] 0 0 0.000000 0 -1 -1 -1 -1 -1 0.0 0 0 0

#> s[6] 0 0 0.000000 0 1 0 0 0 0 0.0 0 0 0

#> s[7] 0 0 0.000000 0 0 1 0 0 0 0.0 0 0 0

#> s[8] 0 0 0.000000 0 0 0 1 0 0 0.0 0 0 0

#> s[9] 0 0 0.000000 0 0 0 0 1 0 0.0 0 0 0

#> s[10] 0 0 0.000000 0 0 0 0 0 0 -0.5 0 0 0

#> x[1] 1 0 1.984229 -1 -1 -1 -1 -1 -1 -0.5 0 0 1

#> u[4] u[5]

#> s[1] 0 0

#> s[2] 0 0

#> s[3] 0 0

#> s[4] 0 0

#> s[5] 1 0

#> s[6] 0 0

#> s[7] 0 0

#> s[8] 0 0

#> s[9] 0 0

#> s[10] 0 1

#> x[1] 1 1

#> Left square root of noise covariance Sigma:

#> u[1] u[2] u[3] u[4] u[5]

#> u[1] 0 0.0 0.0 0.0 0

#> u[2] 0 0.1 0.0 0.0 0

#> u[3] 0 0.0 0.1 0.0 0

#> u[4] 0 0.0 0.0 0.1 0

#> u[5] 0 0.0 0.0 0.0 1

# simulate the time series (with initial states)

out = sim(model, n.obs = 100,

a1 = c(100, 1, # initial states for the trend component

3, 0, # initial states for the cyclical component

5, 10, 10, -10, -10, # ... for the seasonal component

0 # initial state for the AR(1) component

))

# extract the contribution of the respective components

X = cbind(out$y,

out$a[1:100,tmpl$idx$state == 1, drop = FALSE] %*% model$sys$C[1, tmpl$idx$state == 1] +

out$u[,tmpl$idx$noise == 1, drop = FALSE] %*% model$sys$D[1, tmpl$idx$noise == 1],

out$a[1:100,tmpl$idx$state == 2, drop = FALSE] %*% model$sys$C[1, tmpl$idx$state == 2] +

out$u[,tmpl$idx$noise == 2, drop = FALSE] %*% model$sys$D[1, tmpl$idx$noise == 2],

out$a[1:100,tmpl$idx$state == 3, drop = FALSE] %*% model$sys$C[1, tmpl$idx$state == 3] +

out$u[,tmpl$idx$noise == 3, drop = FALSE] %*% model$sys$D[1, tmpl$idx$noise == 3],

out$a[1:100,tmpl$idx$state == 4, drop = FALSE] %*% model$sys$C[1, tmpl$idx$state == 4] +

out$u[,tmpl$idx$noise == 4, drop = FALSE] %*% model$sys$D[1, tmpl$idx$noise == 4])

matplot(X, ylab = 'y', xlab = 't',

type = 'l', lty = 1, col = 1:5)

grid()

legend('topleft', legend = c('y','trend','cycle','season','AR(1) noise'),

lwd = 2, col = 1:5, bty = 'n')

if (FALSE) { # \dontrun{

# the following examples throw errors

# 1 is not a template

cbind_templates(1, tmpl_season(4))

# the respective output dimensions are not equal

cbind_templates(tmpl_season(4), tmpl_stsp_ar(2, 2))

# the third argument is a "VARMA template"

cbind_templates(tmpl_lltm(), tmpl_cycle(1/20,1), tmpl_arma_pq(1, 1, 1, 1))

} # }

# Create a template

tmpl <- tmpl_lltm()

tmpl

#> $h

#> [1] 1 0 1 1 1 0 1 0 0 0 1 0 0 0 0 0

#>

#> $H

#> [,1] [,2]

#> [1,] 0 0

#> [2,] 0 0

#> [3,] 0 0

#> [4,] 0 0

#> [5,] 0 0

#> [6,] 0 0

#> [7,] 0 0

#> [8,] 0 0

#> [9,] 0 0

#> [10,] 0 0

#> [11,] 0 0

#> [12,] 0 0

#> [13,] 1 0

#> [14,] 0 0

#> [15,] 0 0

#> [16,] 0 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 2 2

#>

#> $n.par

#> [1] 2

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Create a template

tmpl <- tmpl_cycle(fr = 1/20, rho = 1)

tmpl

#> $h

#> [1] 1.902113 1.000000 1.902113 -1.000000 0.000000 -1.000000 1.000000

#> [8] 0.000000 1.000000 0.000000

#>

#> $H

#> [,1]

#> [1,] 0

#> [2,] 0

#> [3,] 0

#> [4,] 0

#> [5,] 0

#> [6,] 0

#> [7,] 0

#> [8,] 0

#> [9,] 0

#> [10,] 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 1 2

#>

#> $n.par

#> [1] 1

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Create a template

tmpl <- tmpl_season(s = 4)

tmpl

#> $h

#> [1] -1 1 0 -1 -1 0 1 -1 -1 0 0 -1 1 0 0 1 0

#>

#> $H

#> [,1]

#> [1,] 0

#> [2,] 0

#> [3,] 0

#> [4,] 0

#> [5,] 0

#> [6,] 0

#> [7,] 0

#> [8,] 0

#> [9,] 0

#> [10,] 0

#> [11,] 0

#> [12,] 0

#> [13,] 0

#> [14,] 0

#> [15,] 0

#> [16,] 0

#> [17,] 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 1 3

#>

#> $n.par

#> [1] 1

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Basic example

result <- cbind_templates()

result

#> NULL

if (FALSE) { # \dontrun{

# the following examples throw errors

# 1 is not a template

cbind_templates(1, tmpl_season(4))

# the respective output dimensions are not equal

cbind_templates(tmpl_season(4), tmpl_stsp_ar(2, 2))

# the third argument is a "VARMA template"

cbind_templates(tmpl_lltm(), tmpl_cycle(1/20,1), tmpl_arma_pq(1, 1, 1, 1))

} # }

# Create a template

tmpl <- tmpl_lltm()

tmpl

#> $h

#> [1] 1 0 1 1 1 0 1 0 0 0 1 0 0 0 0 0

#>

#> $H

#> [,1] [,2]

#> [1,] 0 0

#> [2,] 0 0

#> [3,] 0 0

#> [4,] 0 0

#> [5,] 0 0

#> [6,] 0 0

#> [7,] 0 0

#> [8,] 0 0

#> [9,] 0 0

#> [10,] 0 0

#> [11,] 0 0

#> [12,] 0 0

#> [13,] 1 0

#> [14,] 0 0

#> [15,] 0 0

#> [16,] 0 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 2 2

#>

#> $n.par

#> [1] 2

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Create a template

tmpl <- tmpl_cycle(fr = 1/20, rho = 1)

tmpl

#> $h

#> [1] 1.902113 1.000000 1.902113 -1.000000 0.000000 -1.000000 1.000000

#> [8] 0.000000 1.000000 0.000000

#>

#> $H

#> [,1]

#> [1,] 0

#> [2,] 0

#> [3,] 0

#> [4,] 0

#> [5,] 0

#> [6,] 0

#> [7,] 0

#> [8,] 0

#> [9,] 0

#> [10,] 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 1 2

#>

#> $n.par

#> [1] 1

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Create a template

tmpl <- tmpl_season(s = 4)

tmpl

#> $h

#> [1] -1 1 0 -1 -1 0 1 -1 -1 0 0 -1 1 0 0 1 0

#>

#> $H

#> [,1]

#> [1,] 0

#> [2,] 0

#> [3,] 0

#> [4,] 0

#> [5,] 0

#> [6,] 0

#> [7,] 0

#> [8,] 0

#> [9,] 0

#> [10,] 0

#> [11,] 0

#> [12,] 0

#> [13,] 0

#> [14,] 0

#> [15,] 0

#> [16,] 0

#> [17,] 1

#>

#> $class

#> [1] "stspmod"

#>

#> $order

#> [1] 1 1 3

#>

#> $n.par

#> [1] 1

#>

# Use the template with fill_template()

# filled <- fill_template(tmpl, theta = rnorm(tmpl$n.par))

# Basic example

result <- cbind_templates()

result

#> NULL