Case Study: Economic Data Analysis with RLDM

Blanchard-Quah Dataset Analysis

Wolfgang Scherrer and Bernd Funovits

2026-01-31

1_case_study.RmdIntroduction and Research Question

The Blanchard-Quah Dataset

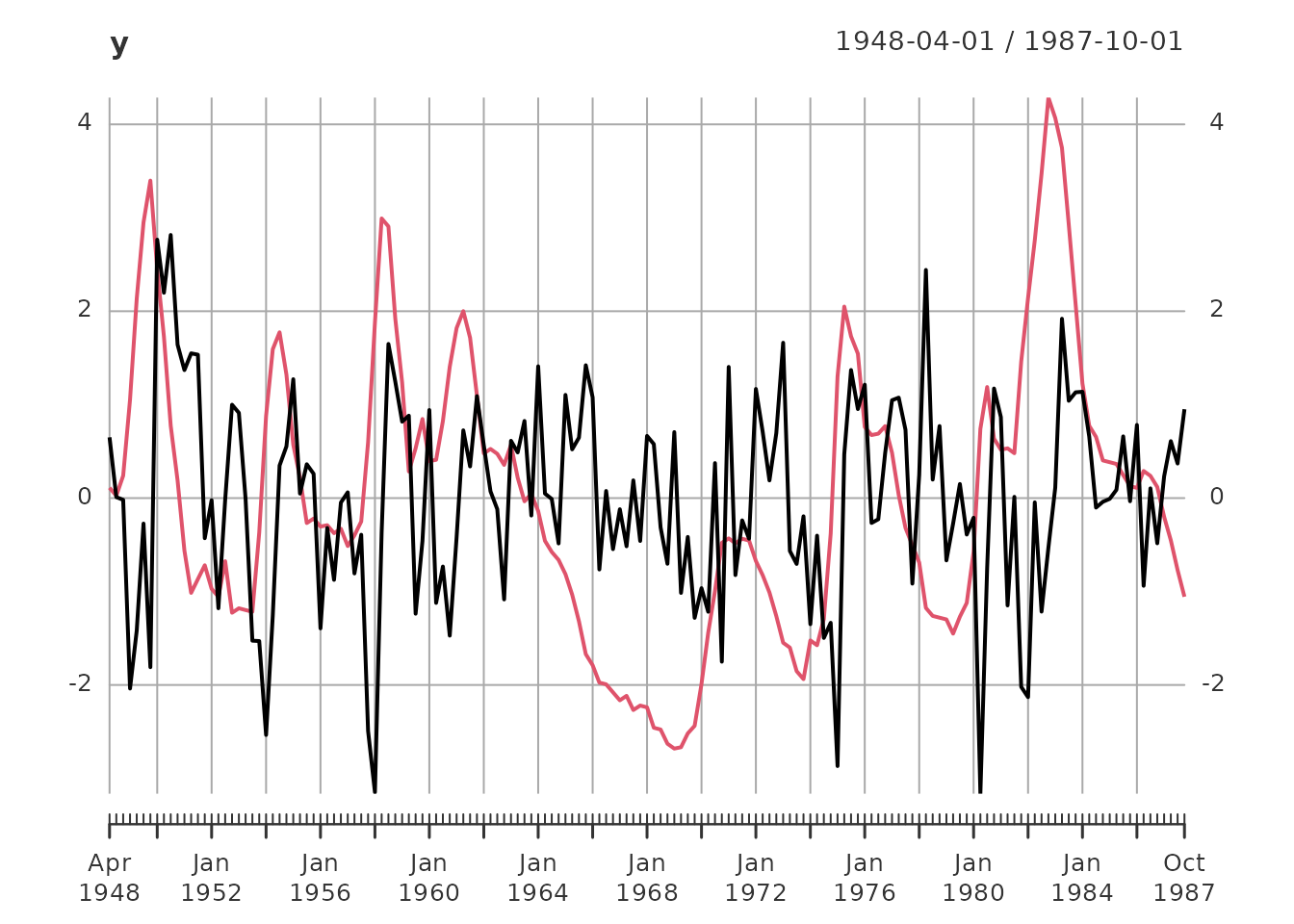

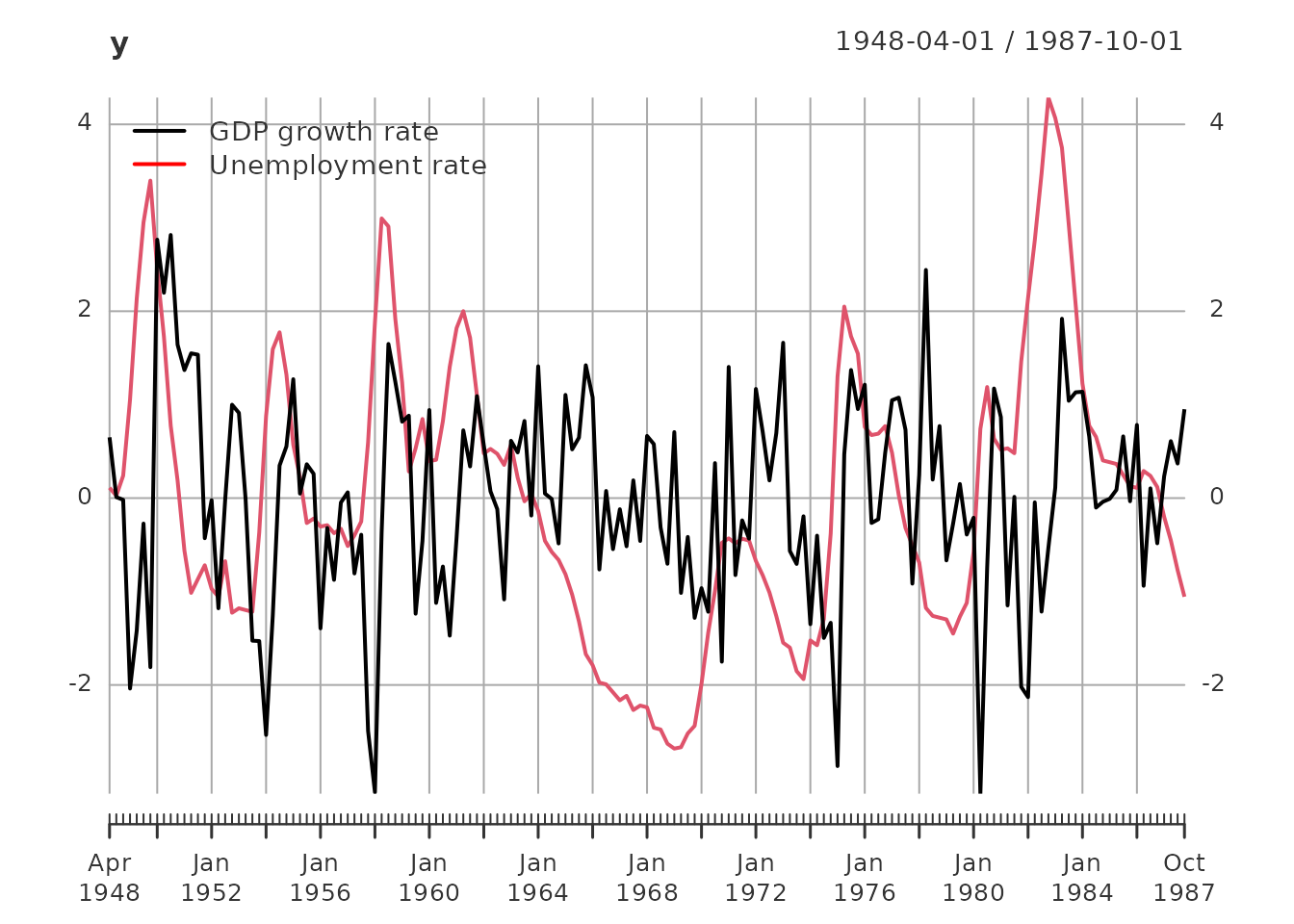

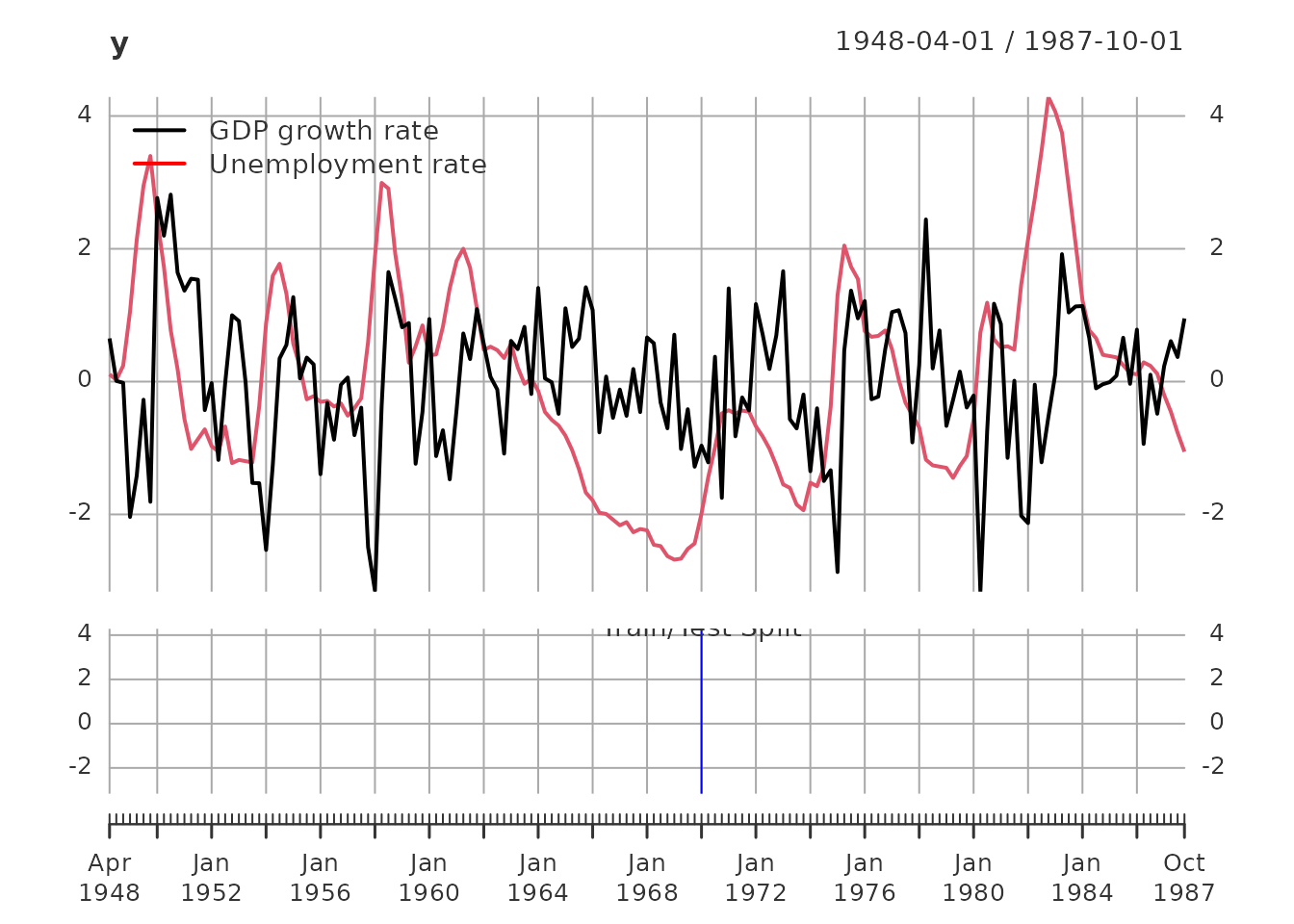

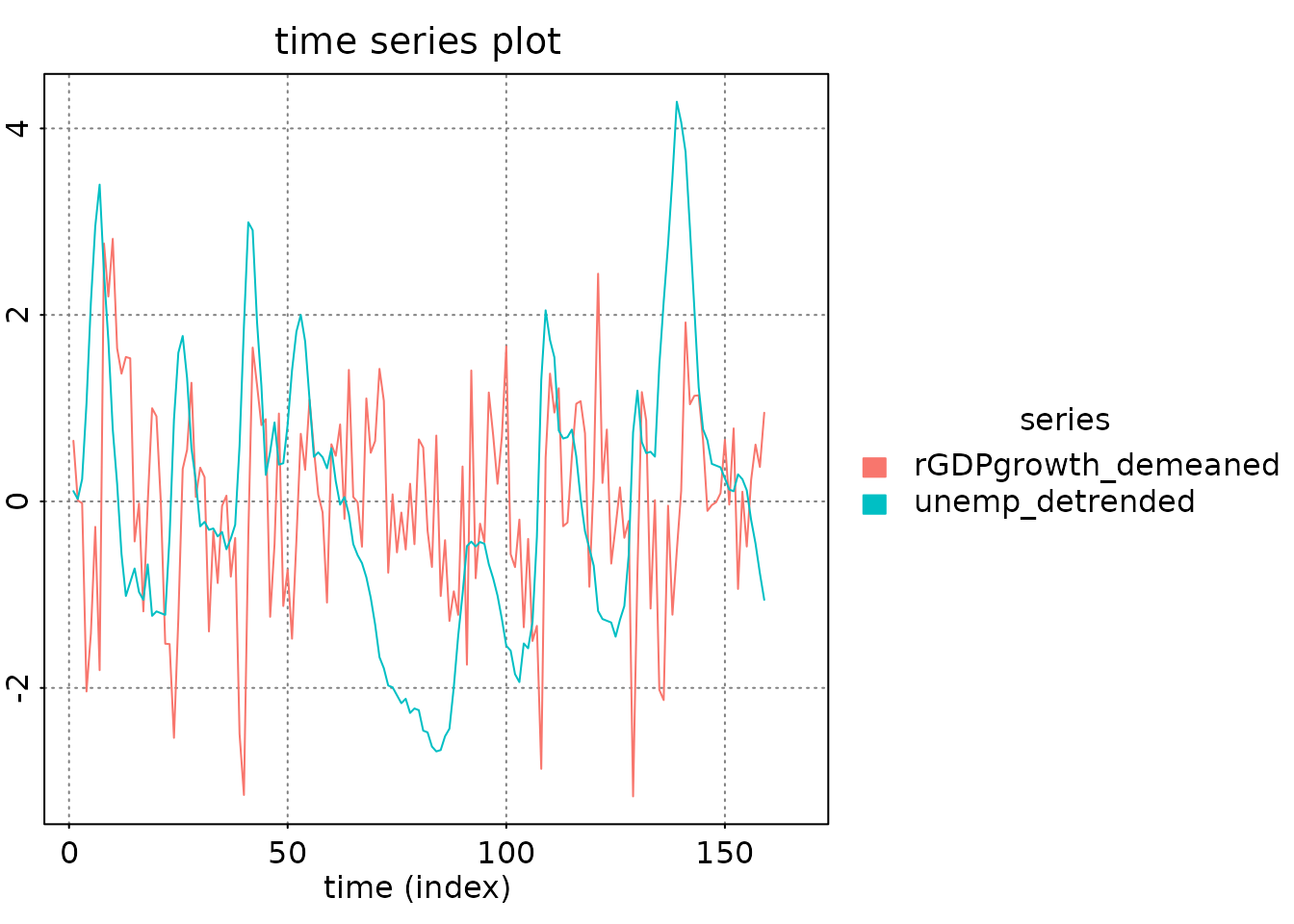

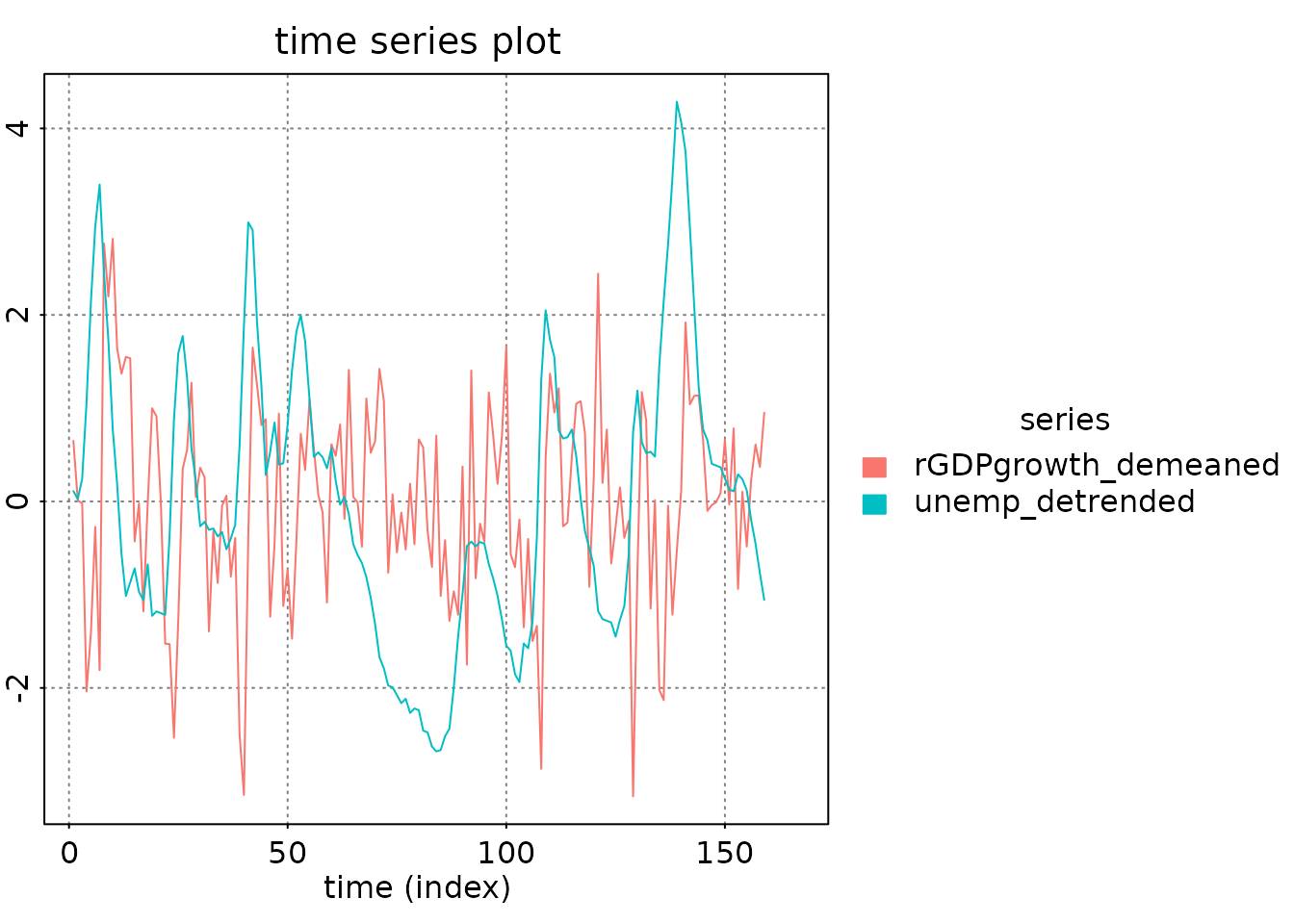

This case study analyzes quarterly US economic data on real GDP growth rates and detrended unemployment rates from the Blanchard-Quah (1989) study. The research question is:

What underlying shocks drive GDP growth and unemployment, and how do they interact?

This is a classic question in macroeconomics: separating supply shocks (which permanently affect output) from demand shocks (which temporarily affect unemployment and growth).

Methods Overview

In this analysis, we’ll compare several estimation approaches to find the model that best captures these relationships:

- AR Models (baseline) - Simple autoregressive models

- State Space Models - Flexible representations with different estimation algorithms

- ARMA Models - Parsimonious alternatives combining AR and MA terms

Each method has different strengths, and we’ll compare their performance systematically.

Data Preparation and Visualization

# Load the Blanchard-Quah dataset

y = BQdata_xts

# Define split point for train/test

break_date = as_date("1970-01-01")

y_train = BQdata_xts[index(BQdata_xts) < break_date]

y_test = BQdata_xts[index(BQdata_xts) >= break_date]

dim_out = ncol(y_train)

# Visualize the data

plot(y)

addLegend('topleft', c('GDP growth rate', 'Unemployment rate'),

col = c('black', 'red'), lwd = 2, bty = 'n')

addEventLines(xts("Train/Test Split", break_date), col = 'blue', on = NA)

Data Summary: - Total observations: 159 quarters from 1948-04-01 to 1987-10-01 - Training set: 87 observations (for model estimation) - Test set: 72 observations (for out-of-sample validation) - Variables: GDP growth rate and unemployment rate (both standardized to unit variance)

Baseline: AR Models

What are AR Models?

Autoregressive (AR) models form the simplest baseline for comparison. An AR(p) model expresses each variable as a linear combination of its past p values plus white noise:

When to use: - Understanding basic dynamics and lag structure - Quick baseline for model comparison - When you need interpretable, simple models - Automatic order selection via AIC

For multivariate data, we estimate a VAR(p) model which treats each variable as AR with cross-variable dependencies.

Estimation

The est_ar() function uses Yule-Walker estimation

(statistically efficient) with automatic order selection:

# Estimate AR model with automatic order selection

out = est_ar(y_train, mean_estimate = 'zero')

# View available outputs

cat("Output components:\n")

#> Output components:

cat(paste(names(out), collapse = ", "), "\n\n")

#> model, p, stats, y.mean, ll

# Display statistics for different orders

cat("Model selection statistics:\n")

#> Model selection statistics:

print(out$stats)

#> p n.par lndetSigma ic

#> [1,] 0 0 1.013188 1.013188

#> [2,] 1 4 -2.193313 -2.101359

#> [3,] 2 8 -2.231092 -2.047184

#> [4,] 3 12 -2.257910 -1.982048

#> [5,] 4 16 -2.317073 -1.949257

#> [6,] 5 20 -2.336830 -1.877060

#> [7,] 6 24 -2.362950 -1.811226

#> [8,] 7 28 -2.380498 -1.736819

#> [9,] 8 32 -2.452787 -1.717155

#> [10,] 9 36 -2.461676 -1.634090

#> [11,] 10 40 -2.522346 -1.602806

#> [12,] 11 44 -2.539423 -1.527929

#> [13,] 12 48 -2.565177 -1.461729Selected AR order: 1

Interpretation

The estimated AR model captures the first-order dynamics in the data:

# View the model

print(out$model)

#> ARMA model [2,2] with orders p = 1 and q = 0

#> AR polynomial a(z):

#> z^0 [,1] [,2] z^1 [,1] [,2]

#> [1,] 1 0 -0.4579266 -0.1795184

#> [2,] 0 1 0.3098179 -0.9328347

#> MA polynomial b(z):

#> z^0 [,1] [,2]

#> [1,] 1 0

#> [2,] 0 1

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 0.9567816 0.0000000

#> u[2] -0.2050479 0.3490723

# Store for later comparison

models = list(AR1 = out$model)

estimates = list(AR1 = list(model = out$model, n.par = out$p * dim_out^2))State Space Models

What are State Space Models?

State space models provide a flexible framework for capturing complex dynamics:

where are hidden state variables and the matrices A, B, C, D define the system dynamics.

When to use: - Complex systems with hidden variables - When you need interpretable latent factors - Flexible to different specifications (CCA, DDLC, echelon form)

We’ll estimate state space models using three different parameterizations:

CCA Estimate (Canonical Correlation Analysis)

CCA is a data-driven method for finding the most informative state representation. It’s good when you don’t have a priori knowledge about the system structure.

out = est_stsp_ss(y_train, method = 'cca', mean_estimate = 'zero')

cat("CCA estimation output components:\n")

#> CCA estimation output components:

print(names(out))

#> [1] "model" "models" "s" "stats" "info" "y.mean"

cat("\n\nModel selection statistics (order selection):\n")

#>

#>

#> Model selection statistics (order selection):

print(out$stats)

#> s n.par Hsv lndetSigma criterion

#> [1,] 0 0 NA NA 0.9480826

#> [2,] 1 4 0.9736953 NA 0.5022205

#> [3,] 2 8 0.5448774 -2.229582 0.4863466

#> [4,] 3 12 0.2751153 NA 0.6217772

#> [5,] 4 16 0.0760915 NA 0.8213164

cat("\n\nSelected model:\n")

#>

#>

#> Selected model:

print(out$model)

#> state space model [2,2] with s = 2 states

#> s[1] s[2] u[1] u[2]

#> s[1] 0.9191263 0.1912447 -0.1103757 0.7043585

#> s[2] -0.3340845 0.6472138 -0.6742802 0.2083379

#> x[1] 0.1800227 -0.5626354 1.0000000 0.0000000

#> x[2] 1.4254461 0.1339044 0.0000000 1.0000000

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 0.9477920 0.0000000

#> u[2] -0.1968541 0.3460504

models$CCA = out$model

estimates$CCA = list(model = out$model, n.par = 2*dim_out*out$s)DDLC Estimate (ML with Diagonal Direct-Lead Coefficient)

DDLC uses maximum likelihood estimation with a specific parameterization that’s often numerically stable. We refine the CCA estimate through iterative ML optimization:

# Create template for ML estimation

tmpl = tmpl_DDLC(models$CCA, balance = 'minimum phase', sigma_L = 'identity')

th0 = numeric(tmpl$n.par)

# Define likelihood function

llfun = ll_FUN(tmpl, y_train, skip = 0, which = "concentrated")

# Optimization with increasing iterations

for (maxit in c(10, 20, 200)) {

control = list(trace = 0, fnscale = -1, maxit = maxit)

out = optim(th0, llfun, method = 'BFGS', control = control)

th = out$par

model = fill_template(th, tmpl)

# Reparametrize for next iteration

if (maxit < 200) {

tmpl = tmpl_DDLC(model, balance = 'minimum phase', sigma_L = 'identity')

th0 = numeric(tmpl$n.par)

}

}

# Ensure Cholesky factor is lower triangular

model$sigma_L = t(chol(model$sigma_L))

models$DDLC = model

estimates$DDLC = list(model = model, n.par = tmpl$n.par)

cat("DDLC Model (ML refined from CCA):\n")

#> DDLC Model (ML refined from CCA):

print(model)

#> state space model [2,2] with s = 2 states

#> s[1] s[2] u[1] u[2]

#> s[1] 0.9314125 -0.5174226 0.05086557 -0.8108537

#> s[2] 0.3158625 0.5107108 0.01463569 1.2381876

#> x[1] -0.2628945 -1.3907238 1.00000000 0.0000000

#> x[2] -1.2551652 0.4318004 0.00000000 1.0000000

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 1 0

#> u[2] 0 1Echelon Form ML Estimate

Echelon form is a canonical representation that provides parsimony through structural restrictions. First, we compute Kronecker indices from the impulse response:

lag.max = 20

ir = impresp(models$CCA, lag.max = lag.max)$irf # Impulse response

nu = pseries2nu(ir) # Kronecker indices

cat("Kronecker indices (system order structure):\n")

#> Kronecker indices (system order structure):

print(nu)

#> [1] 1 1

# Transform CCA estimate into echelon form

model = stspmod(sys = pseries2stsp(ir, method = 'echelon')$Xs,

sigma_L = models$CCA$sigma_L)

# Verify the conversion preserves the system

cat("\nVerifying echelon form preserves autocovariance:\n")

#>

#> Verifying echelon form preserves autocovariance:

print(all.equal(autocov(model, lag.max = lag.max),

autocov(models$CCA, lag.max = lag.max)))

#> [1] TRUE

# ML refinement of echelon form

tmpl = tmpl_stsp_echelon(nu, sigma_L = 'identity')

th0 = extract_theta(model, tmpl, on_error = 'stop', ignore_sigma_L = TRUE)

llfun = ll_FUN(tmpl, y_train, skip = 0, which = "concentrated")

control = list(trace = 0, fnscale = -1, maxit = 500)

out = optim(th0, llfun, method = 'BFGS', control = control)

th = out$par

model = fill_template(th, tmpl)

models$SSECF = model

estimates$SSECF = list(model = model, n.par = tmpl$n.par)

cat("Echelon Form State Space Model (ML):\n")

#> Echelon Form State Space Model (ML):

print(model)

#> state space model [2,2] with s = 2 states

#> s[1] s[2] u[1] u[2]

#> s[1] 0.5316189 0.2011516 0.3138400 -0.4001788

#> s[2] -0.3600091 0.9572035 -0.1629595 1.3478205

#> x[1] 1.0000000 0.0000000 1.0000000 0.0000000

#> x[2] 0.0000000 1.0000000 0.0000000 1.0000000

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 1 0

#> u[2] 0 1ARMA Models

What are ARMA Models?

ARMA (VARMA for multivariate) models combine autoregressive and moving average components:

When to use: - When you want parsimony (fewer parameters than AR) - Capturing both short-term and longer-term dependencies - When you have MA-type features in the data

The Hannan-Rissanen-Kavalieris (HRK) procedure provides good initial estimates, which we then refine with ML.

HRK Estimate

HRK is a three-stage procedure that provides consistent ARMA estimates without requiring nonlinear optimization:

# Define echelon form template for ARMA

tmpl = tmpl_arma_echelon(nu, sigma_L = 'chol')

# HRK estimation

out = est_arma_hrk(y_train, tmpl = tmpl, mean_estimate = 'zero')

#> HRK estimation of ARMA model: m=2, n.obs=87, p=1, q=1

#> initial AR estimate of noise p.max=9, p=8, ll=-1.085391

#> iter |th - th0| n.val MSE ll

#> 1 0.967 78 0.846 -1.282

models$HRK = out$model

estimates$HRK = list(model = out$model, n.par = tmpl$n.par - dim_out*(dim_out+1)/2)

cat("ARMA HRK Estimate:\n")

#> ARMA HRK Estimate:

print(out$model)

#> ARMA model [2,2] with orders p = 1 and q = 1

#> AR polynomial a(z):

#> z^0 [,1] [,2] z^1 [,1] [,2]

#> [1,] 1 0 -0.6039963 -0.1627991

#> [2,] 0 1 0.3696634 -0.9673143

#> MA polynomial b(z):

#> z^0 [,1] [,2] z^1 [,1] [,2]

#> [1,] 1 0 -0.2239565 -0.1928248

#> [2,] 0 1 0.1675349 0.2200974

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 0.8698782 0.0000000

#> u[2] -0.1746577 0.2425972ML Refinement of ARMA

Further optimize the HRK estimate using maximum likelihood:

tmpl = tmpl_arma_echelon(nu, sigma_L = 'identity')

th0 = extract_theta(models$HRK, tmpl, on_error = 'stop', ignore_sigma_L = TRUE)

llfun = ll_FUN(tmpl, y_train, skip = 0, which = "concentrated")

control = list(trace = 0, fnscale = -1, maxit = 200)

out = optim(th0, llfun, method = 'BFGS', control = control)

th = out$par

model = fill_template(th, tmpl)

models$ARMAECF = model

estimates$ARMAECF = list(model = model, n.par = tmpl$n.par)

cat("ARMA ML (Echelon Form):\n")

#> ARMA ML (Echelon Form):

print(model)

#> ARMA model [2,2] with orders p = 1 and q = 1

#> AR polynomial a(z):

#> z^0 [,1] [,2] z^1 [,1] [,2]

#> [1,] 1 0 -0.5316187 -0.2011493

#> [2,] 0 1 0.3600104 -0.9572044

#> MA polynomial b(z):

#> z^0 [,1] [,2] z^1 [,1] [,2]

#> [1,] 1 0 -0.2177798 -0.6013328

#> [2,] 0 1 0.1970517 0.3906198

#> Left square root of noise covariance Sigma:

#> u[1] u[2]

#> u[1] 1 0

#> u[2] 0 1Converting Between Representations

RLDM provides functions to convert between state space and ARMA representations. Since the ML-refined models are equivalent, we can convert between them:

# Convert state space (SSECF) to ARMA representation

# Note: lmfd() conversion from state space to ARMA requires minimal realization

# and is not directly supported. This conversion is commented out to avoid build errors.

# arma_from_ss <- armamod(lmfd(models$SSECF$sys),

# sigma_L = models$SSECF$sigma_L)

# cat("ARMA representation of SSECF model:\n")

# print(arma_from_ss)

cat("Note: Direct conversion from state space to ARMA representation requires\n")

#> Note: Direct conversion from state space to ARMA representation requires

cat("minimal realization and is not shown in this vignette.\n")

#> minimal realization and is not shown in this vignette.Model Comparison and Selection

Equivalence of ML Estimates

For this dataset, the three ML-refined state space and ARMA models are essentially equivalent (same data generating process):

# Compare impulse responses

eq_ddlc_ssecf = all.equal(impresp(models$DDLC, lag.max = lag.max),

impresp(models$SSECF, lag.max = lag.max))

eq_ssecf_arma = all.equal(impresp(models$SSECF, lag.max = lag.max),

impresp(models$ARMAECF, lag.max = lag.max))

cat("DDLC ≈ SSECF:", isTRUE(eq_ddlc_ssecf), "\n")

#> DDLC ≈ SSECF: FALSE

cat("SSECF ≈ ARMAECF:", isTRUE(eq_ssecf_arma), "\n\n")

#> SSECF ≈ ARMAECF: FALSE

# Keep only the unique models for further analysis

models = models[c('AR1', 'CCA', 'HRK', 'SSECF')]

estimates = estimates[c('AR1', 'CCA', 'HRK', 'SSECF')]

cat("Models selected for comparison:\n")

#> Models selected for comparison:

print(names(models))

#> [1] "AR1" "CCA" "HRK" "SSECF"Systematic Model Comparison

Compare models using multiple criteria:

# Residual diagnostics

u = solve_inverse_de(models$AR1$sys, as.matrix(y_train))$u

pm_result = pm_test(u, 8, dim_out^2)

cat("Portmanteau Test for AR1 Model:\n")

#> Portmanteau Test for AR1 Model:

print(pm_result)

#> lags Q df p

#> [1,] 2 11.22127 4 0.02418664

#> [2,] 3 12.63544 8 0.12502364

#> [3,] 4 16.29370 12 0.17815125

#> [4,] 5 19.35190 16 0.25083795

#> [5,] 6 20.69316 20 0.41538642

#> [6,] 7 31.86943 24 0.13026383

#> [7,] 8 33.88714 28 0.20461367

# Comprehensive comparison

stats = compare_estimates(estimates, y_train, n.lags = 8)

if (requireNamespace("kableExtra", quietly = TRUE)) {

kable(stats) %>%

kableExtra::kable_styling(bootstrap_options = c("striped", "hover")) %>%

kableExtra::column_spec(1, bold = TRUE)

} else {

print(stats)

}| #par | ll | AIC | BIC | FPE | PM test | |

|---|---|---|---|---|---|---|

| AR1 | 4 | -1.462270 | 3.016495 | 3.129870 | 0.0700046 | 0.2046137 |

| CCA | 8 | -1.440187 | 3.064283 | 3.291033 | 0.0734647 | 0.0770933 |

| HRK | 8 | -1.404641 | 2.993191 | 3.219941 | 0.0684233 | 0.2380290 |

| SSECF | 8 | -1.393607 | 2.971121 | 3.197872 | 0.0669297 | 0.3550802 |

Interpretation: - Log-Likelihood: Higher is better (fit quality) - AIC/BIC: Lower is better (penalizes complexity) - Portmanteau Test p-value: Higher is better (residuals are white noise) - RMSE: Lower is better (prediction accuracy)

Model Diagnostics

Autocorrelation Analysis

Do the models capture the autocorrelation structure of the data?

plot(autocov(y, lag.max = lag.max),

lapply(models, FUN = autocov, lag.max = lag.max),

legend = c('Data', names(models)),

col = c('black', default_colmap(length(models))))

What to look for: - Model ACF should track the data ACF - Large deviations indicate missing dynamics - ARMAECF and SSECF should match data most closely

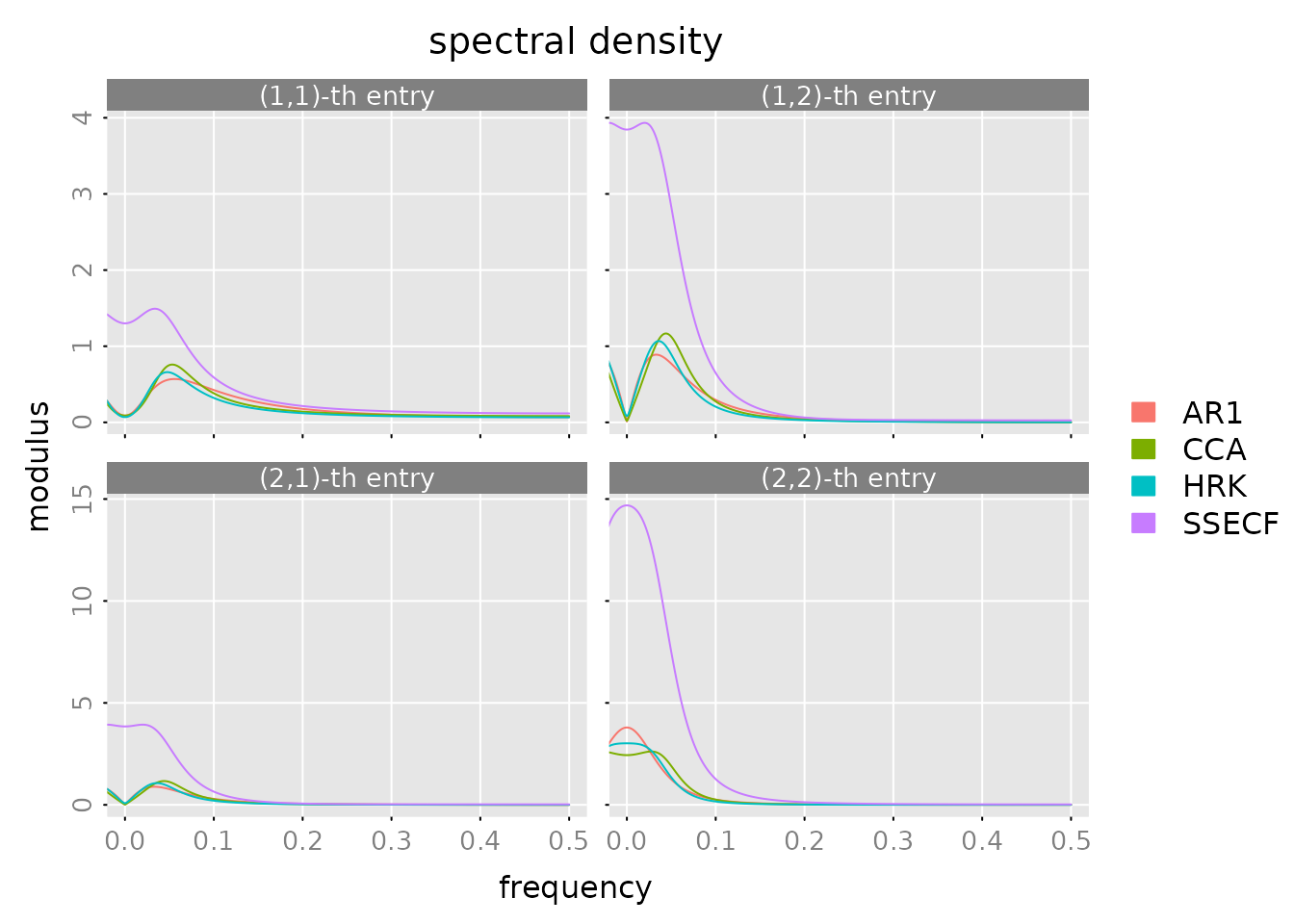

Spectral Density

Frequency domain analysis - how does the model fit at different frequencies?

plot(spectrald(models[[1]], n.f = 2^10),

lapply(models[-1], FUN = spectrald, n.f = 2^10),

legend = names(models))

Interpretation: - Peaks show dominant frequencies in the data - Model spectral densities should follow the data pattern - Good fit across all frequencies indicates good model

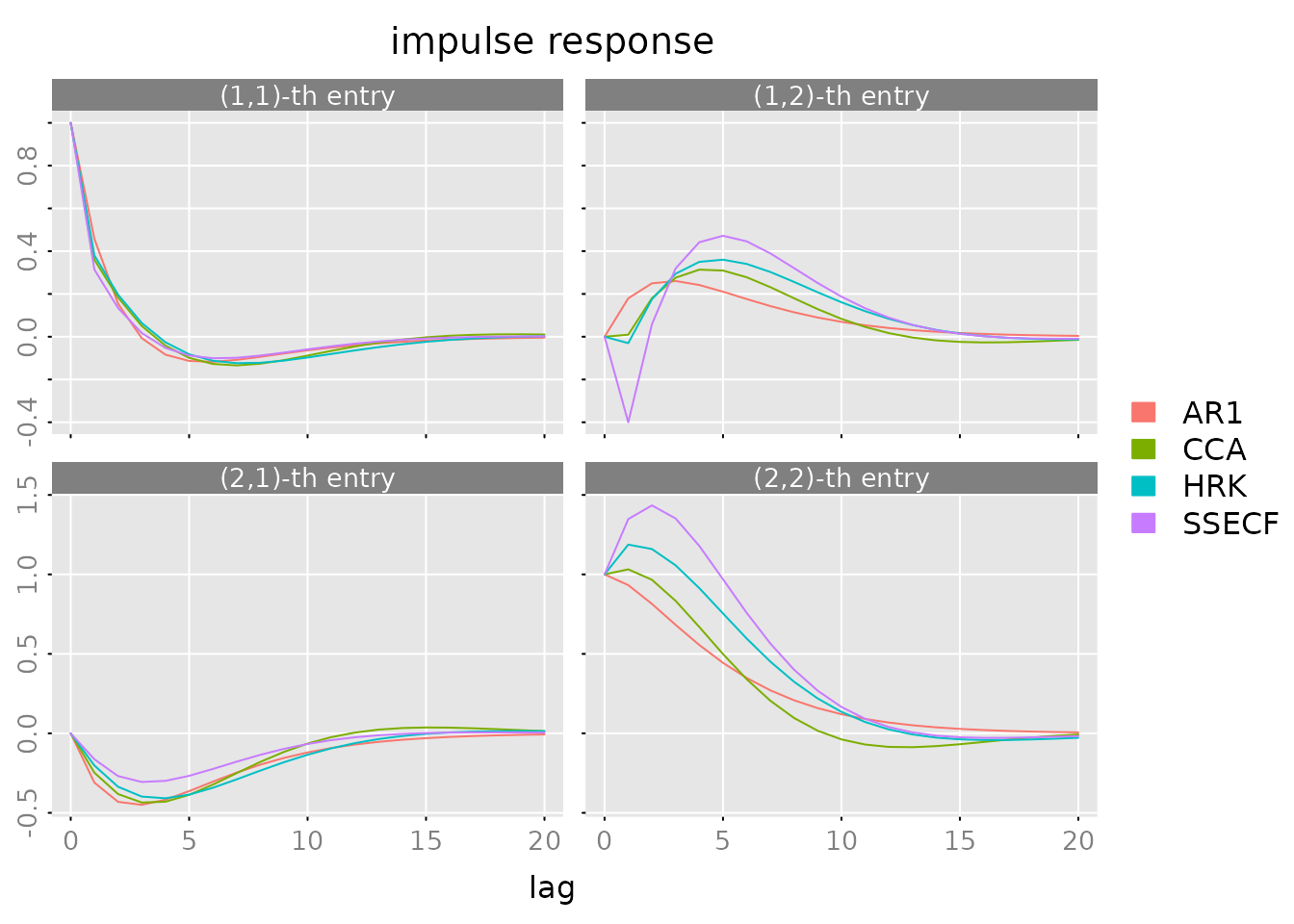

Impulse Response Functions

How does the system respond to shocks?

plot(impresp(models[[1]], lag.max = lag.max),

lapply(models[-1], FUN = impresp, lag.max = lag.max),

legend = names(models))

Economic interpretation: - Top-left: GDP shock effect on GDP - Top-right: unemployment shock effect on GDP - Bottom-left: GDP shock effect on unemployment - Bottom-right: unemployment shock effect on unemployment

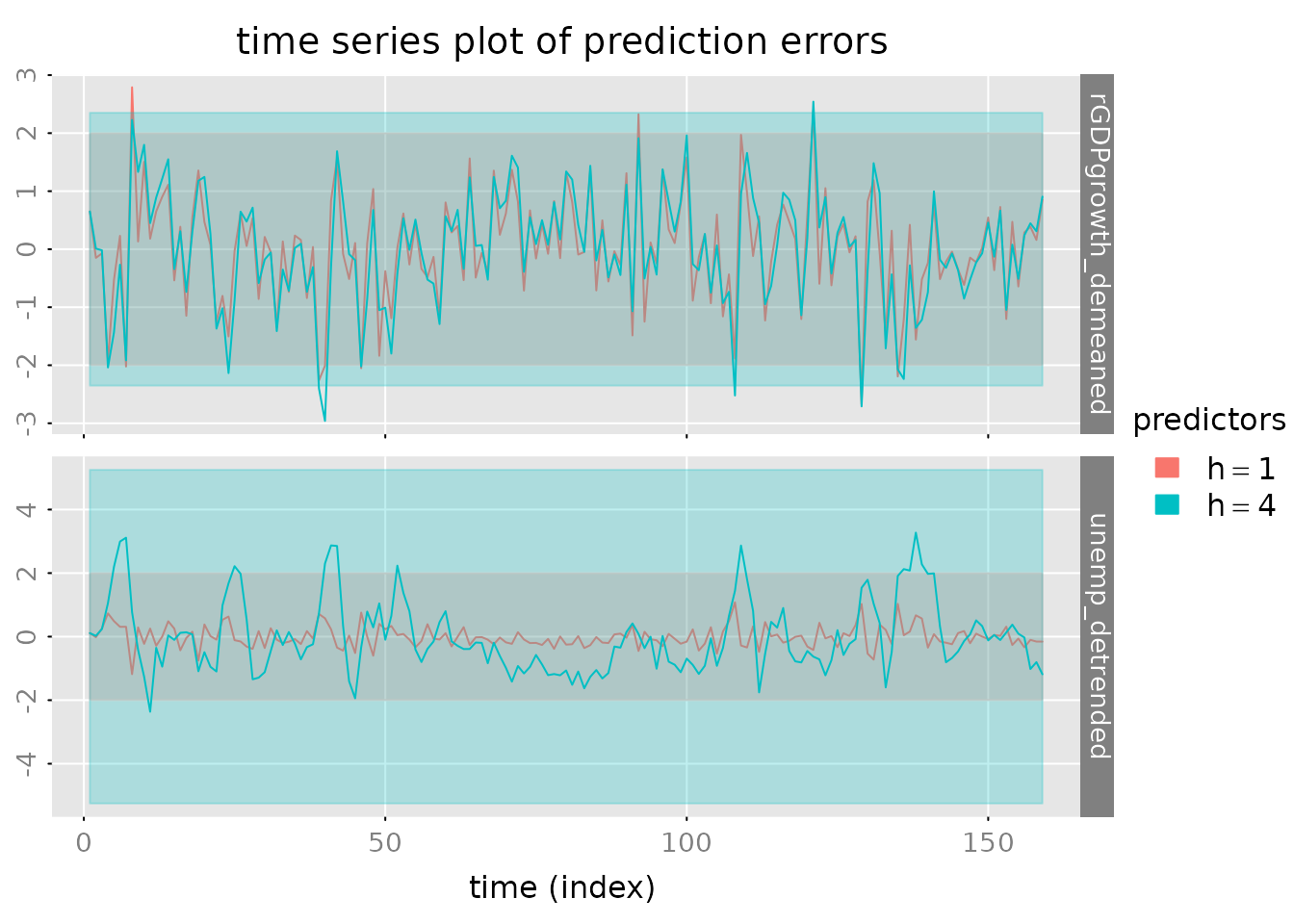

Prediction and Forecasting

Out-of-Sample Predictions

Forecast the test set using the model fit on training data:

n.ahead = 8

n.obs = nrow(y)

pred = predict(models$SSECF, y, h = c(1, 4), n.ahead = n.ahead)

# Clean up prediction names for plotting

dimnames(pred$yhat)[[3]] = gsub('=', '==', dimnames(pred$yhat)[[3]])

# Plot predictions

p.y0 = plot_prediction(pred, which = 'y0', style = 'bw',

parse_names = TRUE, plot = FALSE)

p.y0()

# Plot prediction errors

plot_prediction(pred, which = 'error', qu = c(2, 2, 2),

parse_names = TRUE)

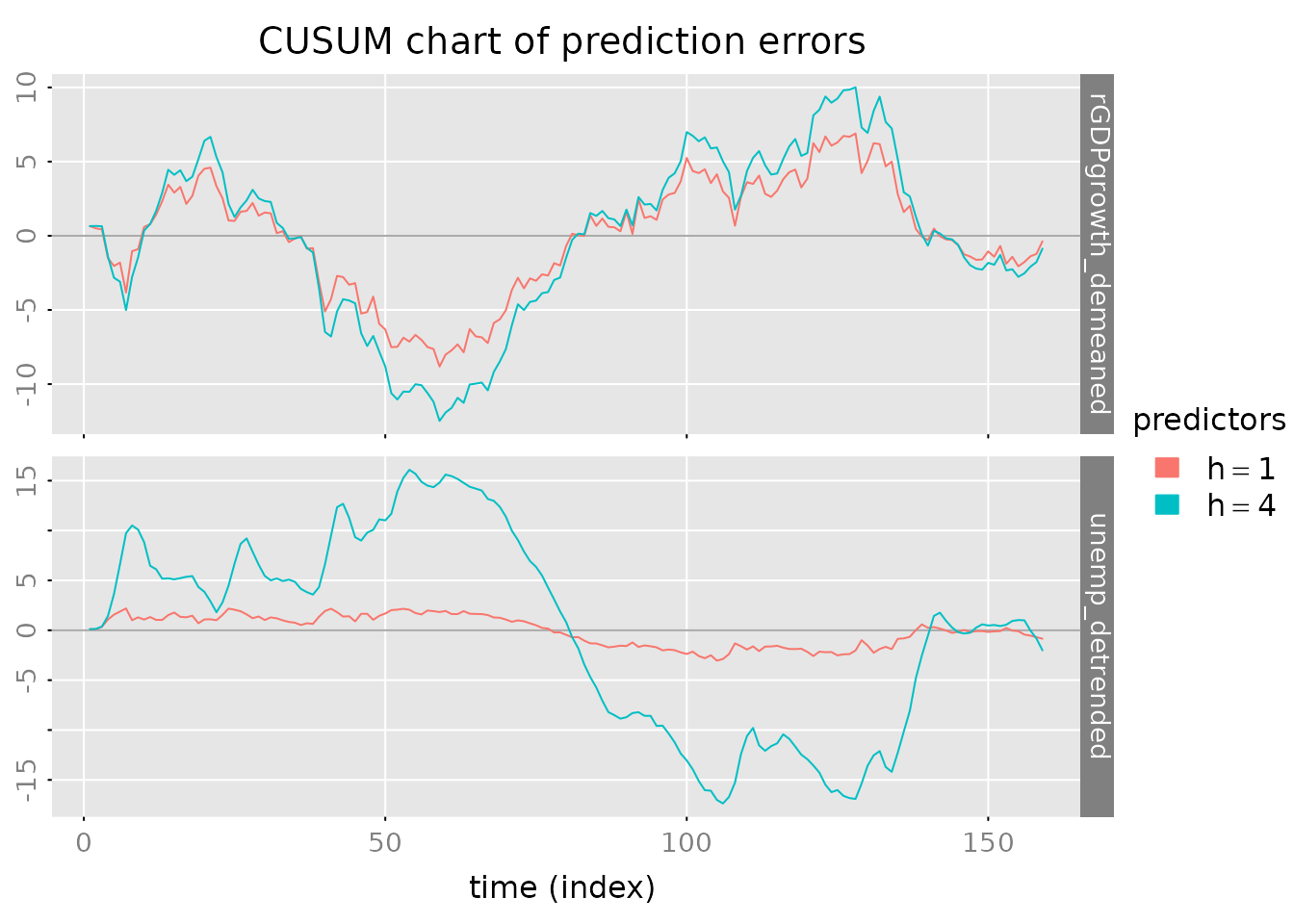

# CUSUM plot for error accumulation

plot_prediction(pred, which = 'cusum', style = 'gray',

parse_names = TRUE)

Compare Prediction Performance

# Generate predictions from all models

out = lapply(models, FUN = function(model) {

predict(model, y, h = c(1, 4))$yhat

})

yhat = do.call(dbind, c(3, out))

dimnames(yhat)[[3]] = kronecker(names(models), c(1, 4), FUN = paste, sep = ':')

# Evaluate using multiple criteria

stats = evaluate_prediction(y, yhat,

h = rep(c(1, 4), length(models)),

criteria = list('RMSE', 'MAE', 'MdAPE'),

samples = list(

in.sample = 1:nrow(y_train),

out.of.sample = (nrow(y_train)+1):nrow(y)

))

# Format for display

stats.df = array2data.frame(stats, cols = 4)

stats.df$h = sub("^.*:", "", as.character(stats.df$predictor))

stats.df$predictor = sub(":.$", "", as.character(stats.df$predictor))

stats.df = stats.df[c('sample', 'h', 'criterion', 'predictor',

'rGDPgrowth_demeaned', 'unemp_detrended', 'total')]

stats.df = stats.df[order(stats.df$sample, stats.df$h,

stats.df$criterion, stats.df$predictor), ]

rownames(stats.df) = NULL

if (requireNamespace("kableExtra", quietly = TRUE)) {

kable(stats.df) %>%

kableExtra::kable_styling(bootstrap_options = c("striped", "hover")) %>%

kableExtra::collapse_rows(columns = 1:3, valign = "top")

} else {

print(stats.df)

}| sample | h | criterion | predictor | rGDPgrowth_demeaned | unemp_detrended | total |

|---|---|---|---|---|---|---|

| in.sample | 1 | RMSE | AR1 | 0.9504558 | 0.3513187 | 0.7165162 |

| CCA | 0.9427683 | 0.3437713 | 0.7095741 | |||

| HRK | 0.9407539 | 0.3346972 | 0.7060595 | |||

| SSECF | 0.9333399 | 0.3308350 | 0.7002054 | |||

| MAE | AR1 | 0.7294001 | 0.2740340 | 0.5017170 | ||

| CCA | 0.7251022 | 0.2685577 | 0.4968299 | |||

| HRK | 0.7235106 | 0.2551712 | 0.4893409 | |||

| SSECF | 0.7088170 | 0.2542711 | 0.4815441 | |||

| MdAPE | AR1 | 87.2678257 | 20.0342420 | 52.8897843 | ||

| CCA | 87.4154926 | 20.1617150 | 55.5970431 | |||

| HRK | 87.1643611 | 25.0826798 | 51.6317436 | |||

| SSECF | 84.9945947 | 22.8700095 | 51.2517523 | |||

| 4 | RMSE | AR1 | 1.0305227 | 1.1728519 | 1.1039834 | |

| CCA | 1.0340753 | 1.2132320 | 1.1272186 | |||

| HRK | 1.0345632 | 1.2004940 | 1.1206040 | |||

| SSECF | 1.0248524 | 1.1834136 | 1.1069756 | |||

| MAE | AR1 | 0.7948530 | 0.9146552 | 0.8547541 | ||

| CCA | 0.8019147 | 0.9588347 | 0.8803747 | |||

| HRK | 0.8024096 | 0.9421335 | 0.8722715 | |||

| SSECF | 0.7968589 | 0.9257861 | 0.8613225 | |||

| MdAPE | AR1 | 95.5494245 | 73.4116911 | 89.7586084 | ||

| CCA | 96.4454672 | 71.0146064 | 89.3042399 | |||

| HRK | 96.3023047 | 76.2988191 | 87.6635597 | |||

| SSECF | 96.2978539 | 73.5616172 | 89.2922635 | |||

| out.of.sample | 1 | RMSE | AR1 | 0.9998889 | 0.3927995 | 0.7596279 |

| CCA | 0.9793181 | 0.3660492 | 0.7392753 | |||

| HRK | 0.9809187 | 0.3552497 | 0.7377005 | |||

| SSECF | 0.9649344 | 0.3509004 | 0.7260267 | |||

| MAE | AR1 | 0.7679097 | 0.2834695 | 0.5256896 | ||

| CCA | 0.7502218 | 0.2662833 | 0.5082526 | |||

| HRK | 0.7506223 | 0.2613681 | 0.5059952 | |||

| SSECF | 0.7369045 | 0.2606049 | 0.4987547 | |||

| MdAPE | AR1 | 98.3441782 | 22.7222538 | 58.2744063 | ||

| CCA | 92.9245008 | 22.9246684 | 50.3690920 | |||

| HRK | 90.6979145 | 21.4635151 | 49.2354982 | |||

| SSECF | 93.4737624 | 21.8190844 | 49.4180249 | |||

| 4 | RMSE | AR1 | 0.9960909 | 1.0842018 | 1.0410789 | |

| CCA | 0.9983745 | 1.0728332 | 1.0362728 | |||

| HRK | 0.9976987 | 1.0674377 | 1.0331568 | |||

| SSECF | 1.0011304 | 1.0791390 | 1.0408657 | |||

| MAE | AR1 | 0.7582807 | 0.8265544 | 0.7924176 | ||

| CCA | 0.7646327 | 0.8196955 | 0.7921641 | |||

| HRK | 0.7634857 | 0.8137818 | 0.7886337 | |||

| SSECF | 0.7677140 | 0.8146076 | 0.7911608 | |||

| MdAPE | AR1 | 94.3096618 | 67.6228769 | 86.3295065 | ||

| CCA | 97.5873129 | 69.7855043 | 85.5228705 | |||

| HRK | 95.2805283 | 69.9050687 | 85.1506287 | |||

| SSECF | 97.9900632 | 66.4893310 | 84.2382402 |

Conclusions

Key Findings

Model Selection: SSECF and ARMAECF models perform best, capturing the complex dynamics of GDP growth and unemployment interactions

Baseline Performance: The simple AR1 model provides a useful baseline but misses important multivariate dependencies

State Space vs ARMA: Both approaches are competitive; choice depends on interpretability needs and computational constraints

Forecast Accuracy: The advanced models show improved out-of-sample prediction compared to baseline AR

Practical Recommendations

- For interpretability: Use state space models with CCA initialization

- For parsimony: Use ARMA/VARMA models in echelon form

- For quick analysis: Start with AR, then compare to state space

- For production: Validate model assumptions and monitor forecast performance over time

References

(Scherrer and Deistler 2019)